Hormuz, Jet Fuel, and the SAF Pipeline: Project-Level Exposure, Feedstock Disruption, and Mandate Risk

Axial Intelligence | SAF Project Tracker | April 2026 | Paid Subscriber Edition

The companion free post established three findings: SAF's relative cost premium over conventional jet fuel has compressed, the Middle East SAF pipeline is directly exposed to the conflict, and policy frameworks face a stress test. This paid edition provides the project-level evidence, the feedstock routing analysis, the mandate-risk framework, and updated scenario modelling.

Premium post contains:

Market Context

Full Middle East SAF Projects Table, and conflict exposure assessment

Feedstock Routing Disruption

Mandate at Risk Assessment

Scenario Analysis: Sustained Disruption vs Recovery

Implications for airlines, investors, feedstock traders, and policymakers.

Data access via premium platform

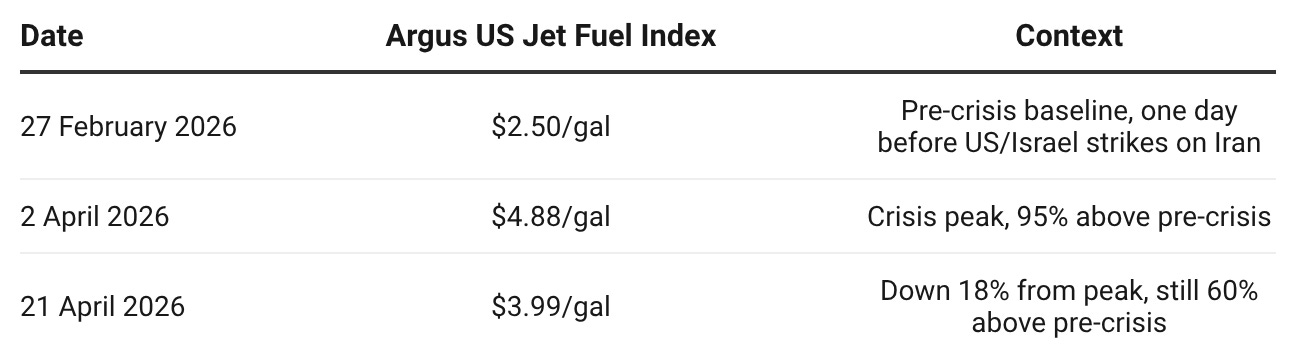

1. Market Context: The Jet Fuel Shock in Numbers

The Strait of Hormuz has been closed since 2 March 2026. On 17 April, Iran announced a brief reopening for the duration of the US-Iran ceasefire. On 18 April, Iran reimposes

restrictions in response to the continued US naval blockade of Iranian ports. The strait remains closed as of 22 April. The closure is now into its eighth week and is the most severe jet fuel supply disruption on record (Al Jazeera, NPR, CNN, 17-18 April 2026).

Key price reference points, using data from the Argus US Jet Fuel Index (simple average of Chicago, Houston, Los Angeles, and New York spot assessments, published under license to Airlines for America):

The decline from $4.88 to $3.99 reflects market response to the brief 17 April Hormuz reopening and to arbitrage inflows from the US and other non-Gulf sources. Prices remain well above pre-crisis levels and the second closure on 18 April has halted the downward move. IEA executive director Fatih Birol warned on 16 April that Europe has approximately six weeks of jet fuel stocks remaining if Hormuz does not reopen. Independent jet fuel stocks at the Amsterdam-Rotterdam-Antwerp (ARA) hub fell to a six-year low in the week ending 15 April (Argus Media).

S&P Global Platts data for 4 March 2026 showed US West Coast conventional jet at $3.59/gallon and California HEFA-SPK SAF at $8.85/gallon, a 147% premium, down from a pre-crisis premium of approximately 223%. SAF prices are driven primarily by feedstock and processing economics (which have risen modestly), while conventional jet is driven by crude oil and refinery utilisation (both severely disrupted). The SAF-to-jet multiple on the 4 March snapshot narrowed from approximately 3.2x to 2.5x.

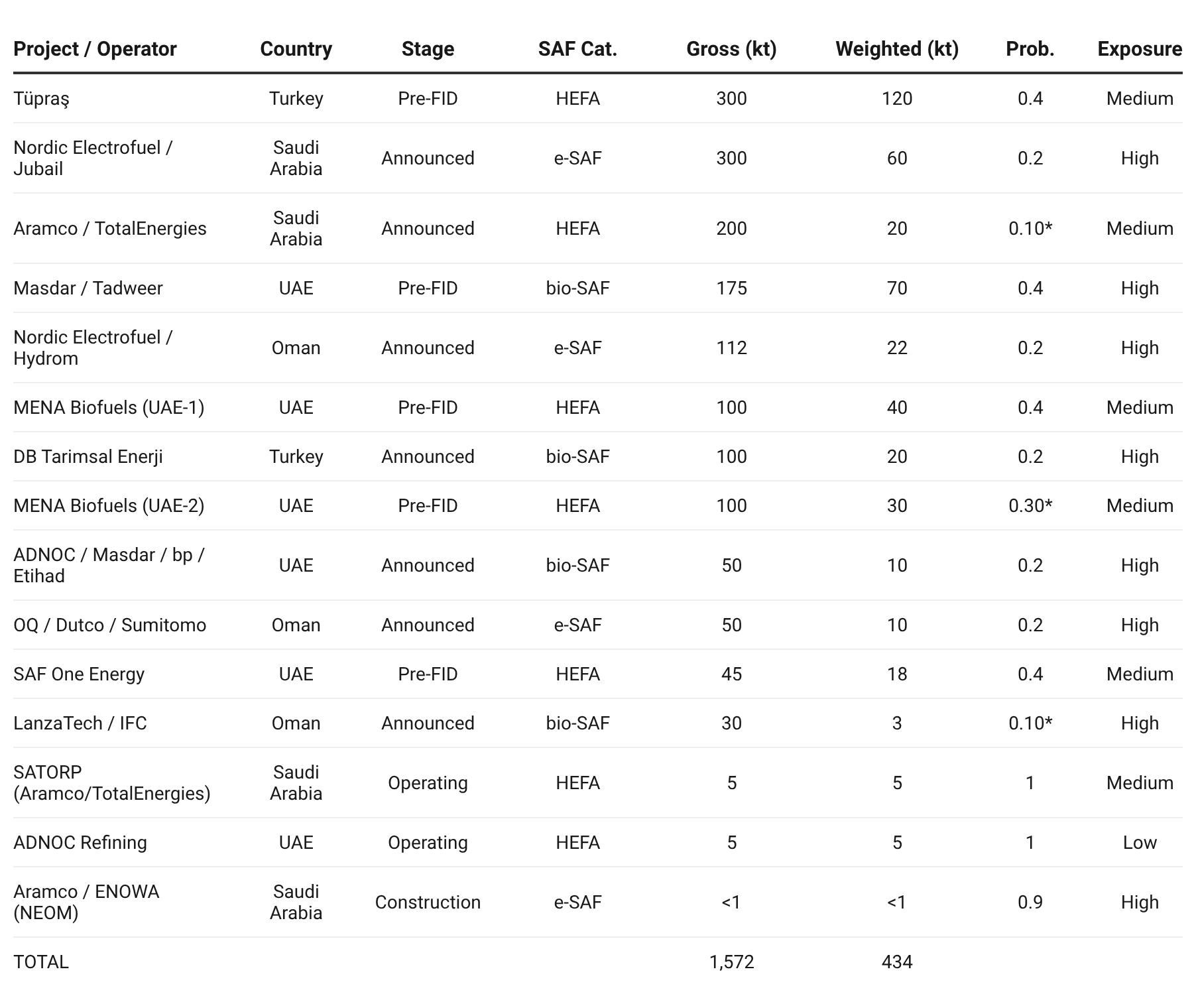

2. Full Middle East SAF Projects Table

All 15 tracked SAF projects in the Middle East, ordered by gross capacity.

Asterisk (*) denotes analyst-adjusted probability below stage baseline. Three projects carry downward adjustments:

Aramco / TotalEnergies / SIRC (Announced baseline 0.20 → 0.10)

MENA Biofuels Fujairah Phase II (Pre-FID baseline 0.40 → 0.30)

LanzaTech / IFC Oman (Announced baseline 0.20 → 0.10)

These adjustments were applied prior to the current conflict based on limited project-specific evidence or elevated developer risk, and reduce the region’s weighted total by 33 kt relative to what stage baselines alone would produce. A pure stage-baseline-weighted total would be approximately 467 kt. Under current conditions, the case for further downward adjustment across the region has strengthened.

Conflict exposure assessment

Turkey (2 projects, 400 kt gross, 140 kt weighted). Sits outside the direct conflict zone but faces elevated energy costs and regional instability risk. Turkish projects are less exposed than Gulf-based facilities. The Tüpraş İzmir project (Pre-FID, 300 kt) is the region’s largest single weighted contributor at 120 kt.

Saudi Arabia (4 projects, 505.5 kt gross, 85.5 kt weighted). Faces direct infrastructure risk. The East-West Pipeline, Saudi Arabia’s primary crude export bypass from the Eastern Province to the Red Sea port of Yanbu, was struck in a drone attack on 8 April, reducing throughput by approximately 700,000 barrels per day. Saudi Arabia announced full-capacity restoration on 12 April (Bloomberg, 8 April 2026; East-West Pipeline operator updates). The SATORP co-processing unit (5 kt operating) is at the Jubail refinery complex on the Gulf coast. The NEOM e-fuel demonstration plant has sub-1 kt disclosed capacity reflecting its pilot-to-commercial phasing and depends on green hydrogen infrastructure at early construction stage.

UAE (6 projects, 475 kt gross, 173 kt weighted). Has experienced direct attacks on port facilities. The Kuwaiti VLCC Al Salmi was struck by an Iranian drone while anchored at the Port of Dubai on 31 March, causing a fire (IRGC claims via Tasnim News Agency; Wikipedia compilation, 31 March 2026). ADNOC Refining’s small co-processing unit (5 kt) is exposed. The Pre-FID projects (Masdar/Tadweer bio-SAF, MENA Biofuels HEFA units) face elevated financing risk as regional capital markets absorb the conflict’s economic impact.

Oman (3 projects, 192 kt gross, 35.4 kt weighted). Geographically adjacent to the strait. All three projects are Announced-stage and carry high exposure scores. Development timelines are likely to extend.3. Feedstock Routing Disruption.

3. Feedstock Routing Disruption

The tracker estimates total feedstock demand from all non-cancelled projects at 63,694 kt/yr, with 26,372 kt (41%) classified as waste oils and fats under the tracker’s normalised primary-feedstock taxonomy. A significant share of global UCO and tallow trade routes through or past the Strait of Hormuz, particularly flows from Southeast Asian collection markets to European HEFA refineries.