The Used Cooking Oil Map: Who Wins, Who Loses, and Who Gets Squeezed by China’s Reopening

The April 2026 reopening of Chinese UCO trade to the United States is a price story on the surface and a project story underneath.

This is the paid companion to “China’s Cooking Oil Is Coming Back to America. The Math Says It Cannot Last.” The free piece set out the headline finding: operating SAF capacity globally already needs more lipid feedstock than China exported in its record year, and the April reopening does not change that.

This brief is the project-level read. It walks through which specific facilities are positioned where, and what each scenario for Chinese UCO flows means for them.

The dataset

The analysis is built on the Axial Intelligence SAF Project Tracker, a structured database of every commercial-stage SAF project globally. The current edition contains 279 projects across 53 countries. Each project carries a full technical and commercial profile: operator, location, technology pathway, feedstock list, capacity, project stage, commissioning probability, source documentation, and last verification date.

For this brief, the relevant subset is the HEFA pathway, which uses lipid feedstocks (UCO, tallow, palm fatty acid distillate, vegetable oils) processed through hydrotreatment. HEFA is the dominant SAF technology today and will remain so through at least 2030. Of the 145 HEFA projects in the Tracker, 126 list UCO or mixed waste oils among their feedstocks. Those 126 projects are the universe for this analysis.

A note on capacity figures used here:

Gross SAF capacity is the total annual SAF output a project would deliver if it commissioned on schedule and ran at nameplate. It is the announcement number.

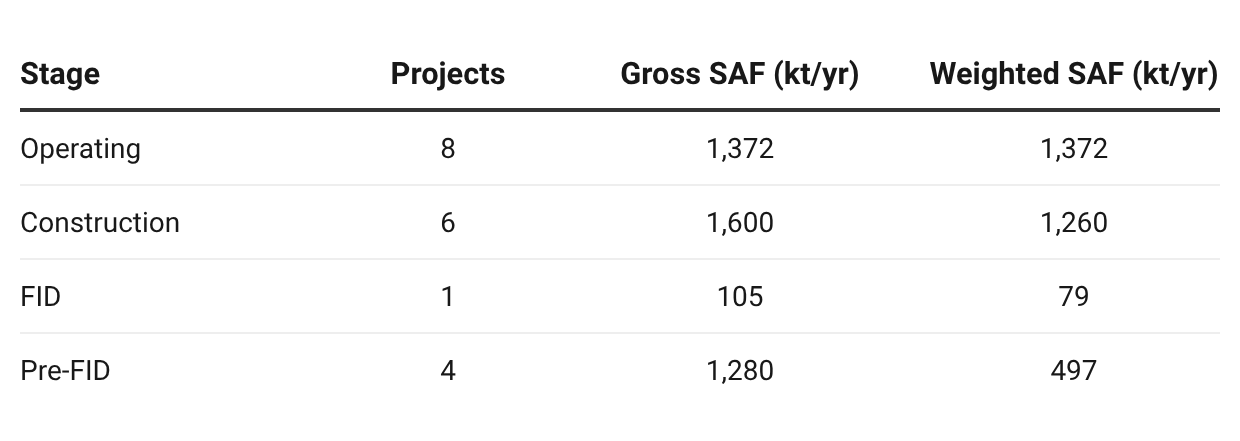

Weighted SAF capacity is gross capacity adjusted for the probability that the project actually commissions. Operating projects sit at 100% probability. Construction-stage projects run at 90% as a baseline. FID-stage at 70%. Pre-FID at 40%. Announced concepts at 20%. Cancelled at 0%. The Tracker also adjusts these baselines up or down on a project-by-project basis where evidence warrants.

Implied lipid feedstock demand is calculated by applying a 1.20 hydroprocessing yield ratio to the SAF capacity. This is the standard industry figure: 1.20 kilograms of lipid feedstock yields 1 kilogram of SAF.

UCO is one of several lipid feedstocks that go into the 1.20 figure. The actual UCO share at any given plant depends on operator sourcing, certification, and price. Those decisions shift in real time. The structural demand for the lipid feedstock category, however, is contracted by the project itself.

The headline numbers

Operating projects alone, with their probability of commissioning fixed at 100% because they are already running, require approximately 7,457 kilotonnes per year of lipid feedstock. That is roughly 2.5 times China’s record 2024 export volume. UCO is a portion of that lipid demand. The rest is covered by tallow, PFAD, and vegetable oils. But the competitive pressure on UCO molecules is set by the size of the lipid pool, not just the share of UCO within it.

Now to the project-level breakdown.

The three buckets

The 126 projects sort cleanly into three strategic groups based on how each is positioned against the China UCO trade flow.

Bucket 1: Inside China (the retention story)

Nineteen Chinese HEFA UCO projects. These are the plants that are taking UCO out of the export pool simply by existing. Combined gross capacity 4,357 kt/yr. Combined weighted capacity 3,208 kt/yr.

Operating and construction-stage Chinese projects together account for 2,632 kt/yr of weighted SAF capacity. At the 1.20 yield ratio, that implies roughly 3,160 kt/yr of lipid feedstock demand inside China. If even half of that is sourced as UCO, the domestic Chinese UCO requirement from this segment alone approaches the entire 2024 Chinese export pool. The construction-stage projects below will commission over the next 24 to 36 months.

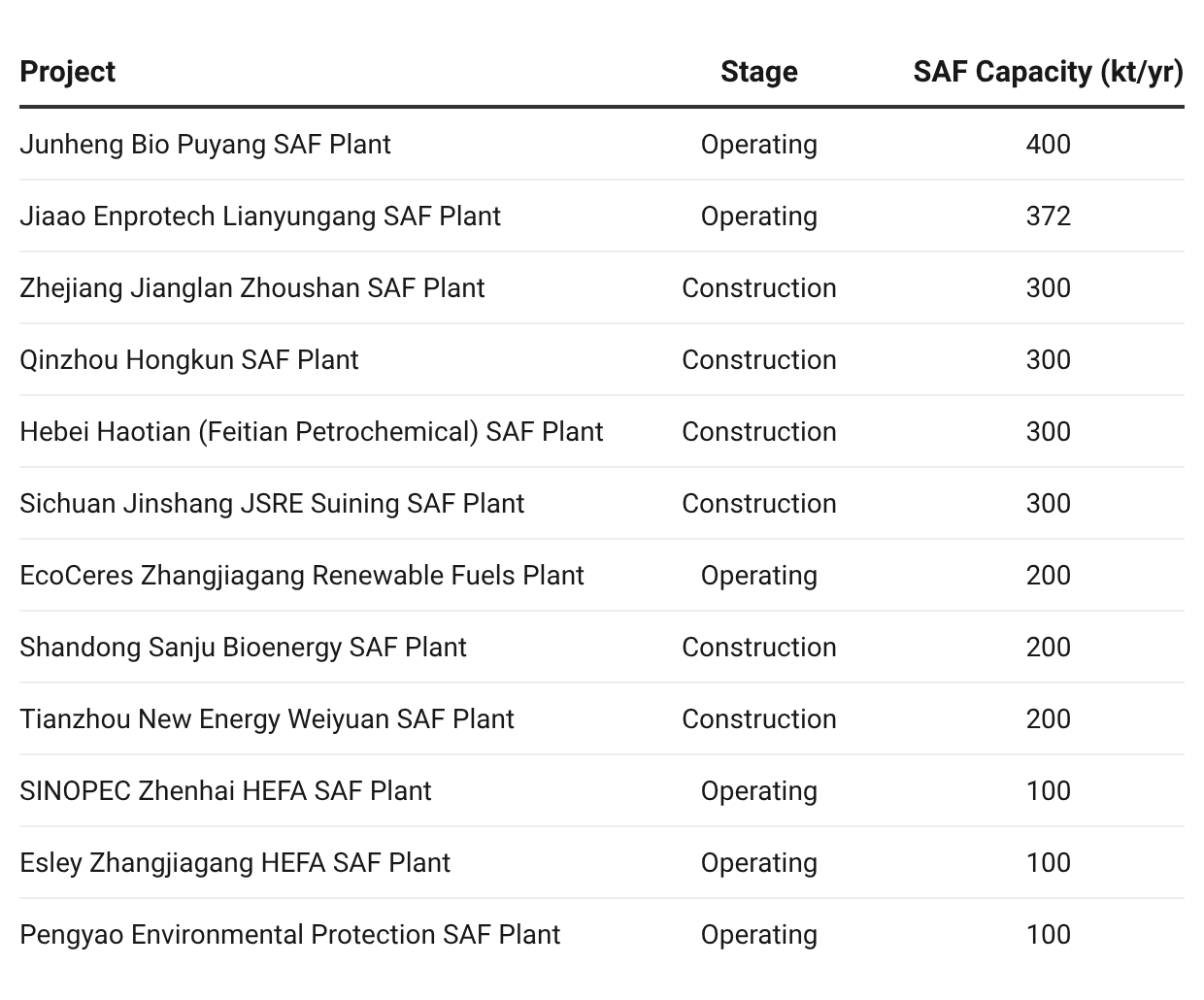

The largest operating and ramp-stage Chinese plants:

SINOPEC Zhenhai is independently RSB-certified. The Chinese ramp pipeline will roughly double the country’s operating UCO-using SAF capacity within three years.

Bucket 2: The United States (the arbitrage beneficiaries)

Nine US HEFA UCO projects. Three are operating. Two are under construction. The remaining four are pre-FID, announced, or on hold. The full US picture: